The Southeast Asia Disaster Risk Insurance Facility (SEADRIF) provides participating ASEAN countries with financial and risk management solutions to strengthen resilience against climate shocks and natural disasters. When disasters strike, economic impacts cascade across governments, businesses, and households, often taking years to recover. Rising disaster frequency and exposure underscore the need for robust fiscal preparedness.

SEADRIF has evolved from concept to capability, delivering fast-disbursing payouts, operational infrastructure, and a collaborative governance framework.

In 2024, SEADRIF formalized its structure through two core entities: the SEADRIF Initiative and the SEADRIF Insurance Company. The Initiative leads governance, strategic coordination, and engagement with members and partners, while the Company delivers technical insurance solutions. Established in 2019 as a general insurer in Singapore and regulated by the Monetary Authority of Singapore, the Company is wholly owned by member countries through the SEADRIF Trust and governed by a professional board.

The Facility’s first catastrophe risk insurance product in the region, co-created with Lao PDR, enabled rapid liquidity for emergency response and early recovery. The success of the product, which has since matured, paved the way for a comprehensive new product with LAO PDR. Supported by the World Bank’s technical expertise and initial capitalization from Japan and Singapore, SEADRIF continues to develop solutions that reduce the financial protection gap and build resilience across Southeast Asia.

SEADRIF and Lao PDR have now introduced a first-of-its-kind parametric insurance policy, the first in the world to use a unique trigger based on the cumulative government - reported number of people affected across several types of disasters. This new model, which reimagines Disaster Risk Financing, can be extended to other countries in the future.

To ensure SEADRIF is focused on serving its member countries and their people, it’s important to define what SEADRIF is not and what it doesn’t do.

After a disaster, countries often face budget constraints and uncertainty over international aid, which can delay or limit support to the most vulnerable communities. Many of these populations lack personal insurance and rely heavily on government-led relief and reconstruction efforts. Without timely support, vulnerable households may resort to harmful coping strategies such as selling productive assets or withdrawing children from school, erasing years of progress. By having disaster response plans and pre-arranged funding in place before disasters strike, SEADRIF enables governments to act quickly. Its insurance payouts provide a predictable and timely source of funding, helping accelerate emergency relief and recovery efforts that protect those who need it most.

SEADRIF has received grant funds for three purposes: 1) initial capitalization; 2) operating expenses; and 3) technical services and risk management support to member countries. These grants are funded by Japan and Singapore. The premiums for insurance policies are paid by the respective policyholders or their supporters.

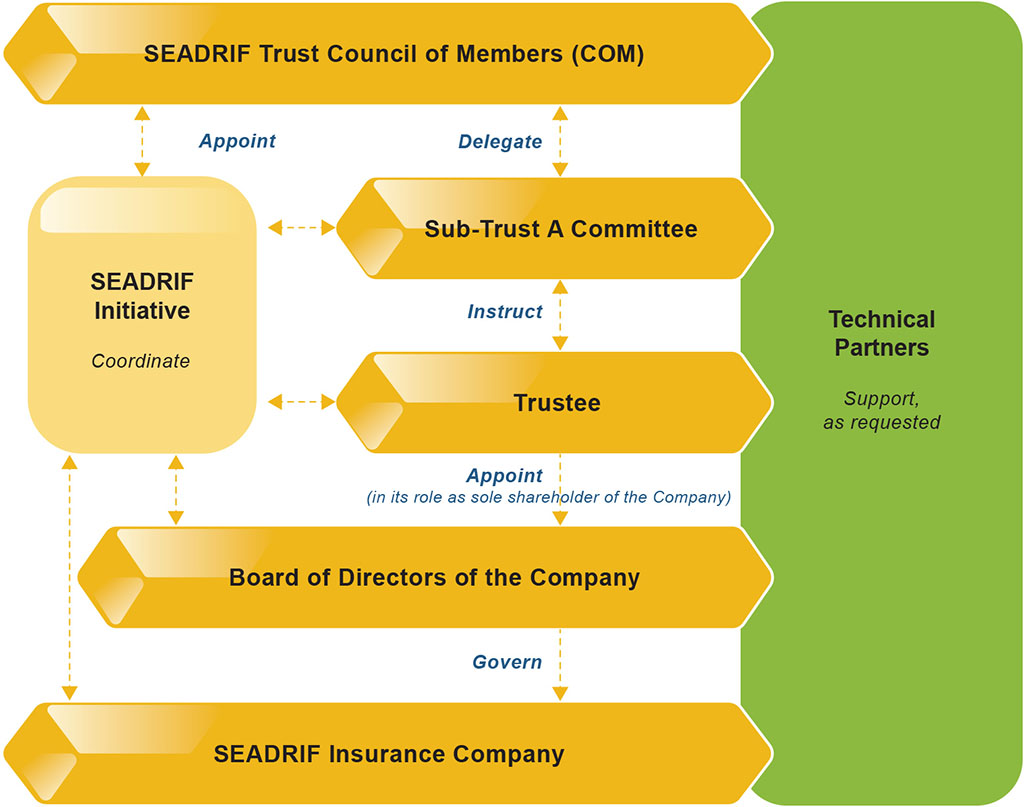

The SEADRIF Initiative comprises four-tiers: 1) the SEADRIF Trust, 2) the Sub-Trust A (created for the SEADRIF Insurance Company), 3) the Trustee, and 4) the Insurance Company.

SEADRIF Stakeholder groups:

SEADRIF’s first insurance product for Lao PDR provided innovative flood protection using a parametric trigger based on modelled estimates of people affected, with payouts tied to specific disaster severity levels. However, due to challenges in matching impact on the ground through the modelled approach, SEADRIF and Lao PDR have now co-created a global first-of-its-kind parametric insurance policy that combines several groundbreaking features: it uses official disaster impact data reported directly by Lao PDR’s National Disaster Management Office (NDMO), offers multi-peril coverage beyond floods, and spans multiple years.

This unique policy triggers payouts when the total number of people affected by disasters reaches agreed thresholds within each 12-month period. Unlike traditional parametric insurance that relies on hazard data or proxies, this policy grounds its triggers in government-verified reports, ensuring accuracy and alignment with national disaster management practices. Payouts are disbursed progressively as thresholds are crossed, allowing Lao PDR to receive timely financial support not only for large catastrophes but also for the cumulative impact of smaller, more frequent events. Funds are typically released within 10 business days after information is received about the number of people impacted on the ground, providing rapid liquidity to accelerate emergency response and recovery efforts, and enhancing the government’s ability to protect vulnerable populations.

This is the first sovereign parametric insurance policy to use government-reported population impact data—rather than hazard intensity or modelled losses—as the sole trigger for payouts. Fully integrated with Lao PDR’s legal and institutional frameworks, it leverages the NDMO’s post-disaster reporting system under the national Disaster Management Law. This means that the trigger reflects Lao PDR’s own definition of people affected rather than abstract technical estimates. By aligning with the national disaster reporting system, the policy strengthens institutions, builds local ownership, reduces basis risk, and grounds payout expectations in government processes.

The policy offers multi-peril coverage in a single contract, covering the full range of hazards most likely to affect the country. It is also multi-year, providing continuity and predictability across disaster seasons. The annual aggregation feature addresses a critical gap in risk financing by allowing cumulative impacts of multiple small and medium-sized events to trigger payouts. Progressive payout based on predefined thresholds ensure timely liquidity for the government.

Parametric insurance determines payout amounts based on predefined estimations of the severity of a disaster event, rather than on actual loss assessments.

The new product builds on this foundation but takes the parametric model a step further by linking payouts directly to the actual number of people affected by disasters over a 12-month period. Instead of relying primarily on hazard or modelled data, this policy uses formal disaster impact reports submitted by Lao PDR’s National Disaster Management Office (NDMO), which operate according to national law and established procedures.

The payouts are triggered progressively as thresholds are crossed. This allows the government to access financial support not only for large-scale catastrophes, but also for the cumulative toll of smaller disasters over time. Because the NDMO reporting process begins as soon as a disaster unfolds, the policy can trigger payouts while events are still ongoing. Once a threshold is met, funds are calculated after verification by the calculation agent of the number of people affected and disbursed within 10 business days. This structure ensures transparency, simplicity, timely liquidity, and alignment with the way Lao PDR manages disaster impacts.

Previously, in its first product, the core of this parametric approach was the SEADRIF Flood Risk Monitoring Tool. This tool provided near real-time assessments of a flood’s magnitude and potential impact by combining multiple data sets. It estimated the severity of the flood event in terms of return periods — for example, a medium-scale event might be classified as a 1-in-8 year occurrence (meaning an event of this severity or worse happens on average every 8 years), while a severe event might be a 1-in-20 year occurrence. Based on these thresholds, beneficiaries received predetermined payouts.

Basis risk occurs when the trigger used to determine insurance payouts does not perfectly match the actual losses experienced. This is inherent in all parametric insurance because payouts are based on pre-set models or proxies rather than direct loss assessments. For example, a severe disaster might cause significant losses but not trigger a payout (negative basis risk), or a minor event could trigger a payout despite limited damage (positive basis risk). In its earlier product for Lao PDR, SEADRIF calibrated its Flood Risk Monitoring Tool and parametric thresholds carefully using historical events to reduce this risk, but it was still observed over the course of the policy.

As no model is perfect and due to challenges in capturing actual impacts through the modelled approach, SEADRIF and Lao PDR co-created the world’s first sovereign parametric insurance policy that uses government-reported population impact data as the sole trigger for payouts—rather than relying on hazard intensity or modelled losses. This policy is fully integrated into Lao PDR’s legal and institutional frameworks, leveraging the National Disaster Management Office’s (NDMO) official post-disaster reporting system under the national Disaster Management Law. As a result, the trigger reflects Lao PDR’s own definition of people affected instead of abstract technical estimates.

The new product significantly reduces basis risk by using Lao PDR’s official disaster impact reports—specifically, the number of people affected—as the trigger for payouts, instead of relying on modelled hazard data or proxy measures. Because it’s tied directly to government-verified data on actual disaster impacts, the policy aligns payouts more closely with real losses experienced on the ground. This approach improves accuracy, builds local ownership, and ensures that funds are released based on the country’s own assessment of disaster severity, minimizing the chance of payouts not matching actual needs.

Unlike traditional indemnity insurance, the countries determine how much premium they can pay, and the SEADRIF Insurance Company calculates the level of coverage it can offer in return. SEADRIF calculates coverage based on several factors:

This approach ensures flexibility for member countries, while maintaining affordability and transparency in how premiums translate into financial protection.

Payouts are made directly by SEADRIF Insurance Company to the insured country and are managed through the government’s own systems and processes. In the case of the policy to Lao PDR this supports emergency response and early recovery.

Reinsurance ensures that the SEADRIF Insurance Company can meet eligible claims with timely payouts, even in years with severe disaster events. It maximizes the efficient use of capital and enhances SEADRIF’s ability to offer higher coverage limits. SEADRIF partners with private reinsurers on commercial terms to support the long-term financial sustainability of the initiative.

To sustain protection for its member countries over the long term, SEADRIF has put in place robust systems that ensure its products work optimally, with transparency and sound governance. The initiative is not managed for profit. Any income or capital is redeployed exclusively to achieve SEADRIF’s sole objective: providing financial protection to its member countries.

Organizational Oversight and Governance

Payout Management and Accountability

SEADRIF aims to maintain a transparent and simple payout structure, putting people first in its bid to provide disaster risk insurance across the region.

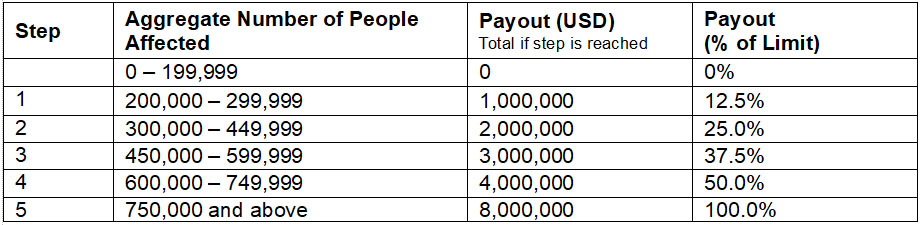

Under the new product policy conditions, payouts are triggered by the cumulative number of people affected by covered disasters (flood, tropical cyclone, earthquake, landslide, and ensuing perils) during each 12‑month policy period, as reported by the Government of the affected country and verified by Gallagher Re, the calculation agent. As cumulative impact thresholds are crossed, portions of the annual aggregate limit (USD 8 million) are released on a progressive schedule:

Payouts are calculated each time a new threshold is reached and disbursed within 10 business days after verification by the calculation agent of the number of people affected. Because the trigger aggregates all reported people affected across events, the policy can respond to both major catastrophes and the cumulative toll of smaller disasters; the government provides information on the number of people impacted for all scales of disasters. It resets each 12‑month period within the two‑year policy term. Funds are allocated in line with a pre‑agreed contingency plan to support emergency response and recovery.

SEADRIF is building a track record of disbursing payouts quickly and effectively. In response to the flooding and damage caused by Typhoon Yagi in Lao PDR in September 2024, SEADRIF provided vital payouts within a short window. On September 20, just five days after the flooding reached its first peak, an initial payout of $750,000 was disbursed to the Ministry of Finance. An additional transfer of $2.25 million was made a week later as additional parts of the country were affected.

In the new policy, payouts are calculated each time the cumulative number of people affected crosses a predefined threshold and are disbursed within 10 business days. Because reporting by national disaster management agencies begins as events unfold, payouts can be triggered while disasters are still ongoing. Funds are transferred to the Ministry of Finance and then allocated through government systems in line with a pre‑agreed Contingency Plan to support emergency response and recovery, meeting agreed fiduciary and environmental/social safeguards.

A payout under the parametric component is made as long as the event meets the criteria outlined in the insurance policy. Like any insurance, however, there are circumstances that do not qualify for a payout.

Under the most recent policy, if the aggregate number of people affected by disasters over a period of 12 months is less than 200,000, there will be no payout according to the conditions of the policy.

SEADRIF products are not directly available to the public. They are designed primarily to support national governments of ASEAN countries in managing disaster relief and recovery. However, where aligned with SEADRIF’s development mandate, the Company may also provide coverage to other public or development-focused entities that fulfill a clear public good need or serve vulnerable populations within ASEAN. This approach ensures that SEADRIF’s resources are directed towards maximizing social impact and resilience across the region.

SEADRIF is the first dedicated regional insurance facility for governments that tackles natural and climate disasters in Southeast Asia. Globally, similar solutions include CCRIF SPC (formerly the Caribbean Catastrophe Risk Insurance Facility Segregated Portfolio Company), the African Risk Capacity Ltd (ARC) and the Pacific Catastrophe Risk Insurance Company (PCRIC). Some countries have also established dedicated insurance facilities domestically, such as the Japan Earthquake Reinsurance or New Zealand’s Natural Hazards Commission (NHZ).

SEADRIF was established by ASEAN+3 member countries as a regional platform to strengthen financial resilience against disasters. It is open to all ASEAN countries and offers flexible coverage that can be tailored to each country’s specific needs — including the types of disasters covered, payout triggers, and desired levels of protection. The SEADRIF Insurance Company is also exploring additional products to provide expanded and innovative risk financing solutions for its members.